Markets have been in “wait-and-see” mode this week, ahead of a “wait-and-see” Fed perhaps. The “transitory inflation” story is now fully priced in (after a few moments of disbelief) by markets which means the Fed may struggle to be any more dovish at their meeting this evening. Is it now time to acknowledge that some of the emergency bond buying programmes for the pandemic depression are not needed in a few months? At least some consideration of the timing of the taper seems warranted, as traders obsess over the “t” words.

The dollar has been firm this week, though closing within ranges with two “doji” candles printing so far. Trends have been mixed across G10 pairs with trading generally quiet as traders await the dots and hang on every word and change in language from Jay Powell and the FOMC.

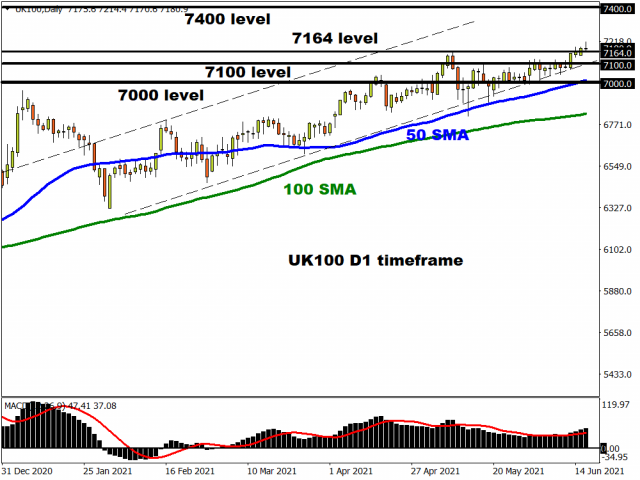

More upside to come in the FTSE100

Stocks are treading water with US futures mixed and European markets opening modestly higher. The FTSE 100, sometimes known as the “global cyclical bellweather” due to the majority of the listed companies generating revenues from overseas, is aiming to push higher as it still lags other major indices in making new all-time highs. A strong close this week will put bulls in the box seat for more upside, with targets above being 7400 which would be close to reclaiming all the losses from the pandemic selloff.

The UK released inflation data earlier this morning with you guessed it, beats across the board! The headline number came in at 2.1% y/y versus analyst estimates of 1.8% while the core also printed stronger than expected at 2.0% against the 1.5% projection. Hot numbers for sure, with the usual base effects and supply constraints in the price pressure mix. BoE policymakers will be alert to this in the general narrative of rising prices.

Oil marches higher

Brent crude is trading above $74 and at levels last seen back in April 2019. API reported overnight that US crude oil inventories fell by 8.5 million barrels over the last week, far more than the 2.5 million barrels decline the market was expecting. If the EIA reports a similar fall later today, it would be the largest decline wince the start of the year. Optimism over the demand outlook is one factor driving prices north, while both OEPC+ and US shale oil producers are expected to support the supply of oil.

Exención de responsabilidad: El contenido de este artículo incluye opiniones personales, y no debe ser interpretado como asesoramiento sobre inversión personal y/o de otro tipo y/o una oferta y/o solicitud de ninguna transacción con instrumentos financieros y/o garantías y/o pronóstico de rendimiento futuro. ForexTime (FXTM), sus afiliados, agentes, directores, responsables y empleados no garantizan la precisión, validez, puntualidad o compleción de ninguna información o dato disponible, y no asume ninguna responsabilidad por cualquier pérdida que resulte de cualquier inversión realizada en base a ellos.