The markets are beginning to increasingly look through the two-party debate over new fiscal stimulus and along with the easing concerns around a contested election result, there’s an upbeat mood on Wall Street. As the Democratic challenger’s lead widens in the polls, hopes are rising that his party, which has already agreed a $2.2 trillion recovery package, could take control of both houses and open the spending taps within the first hundred days of his Presidency.

The Dollar is fairly listless against the majors with volatility drifting somewhat and most currencies holding within their established ranges. Of course, uncertainty around the US election is never far away and with just a few weeks left until polling day, we can’t rule anything out, especially when the incumbent and former reality TV star is struggling not to become one of only four other one-term Presidents in the last hundred years.

The ECB Minutes released earlier in the morning session stated that Euro appreciation has had a material impact on the inflation outlook. They also suggested that policymakers were in no hurry to increase the size of their bond buying programme. Interestingly, bond yields in the peripheral Eurozone countries continue to hit record lows with the Italian 10-year yield last night closing at the same level as the benchmark US 10-year Treasury yield.

Q3 Earnings next week

Companies listed on the S&P500 are set to report a big year-on-year decline in earnings of potentially over 20%, which could be their worst performance since the second quarter of 2009 at the height of the credit crisis. However, this nadir should be followed by a recovery triggered by jumbo-sized policy support.

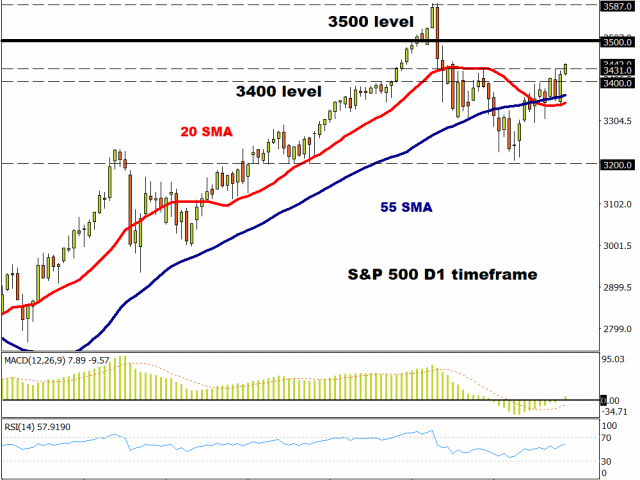

Technically, the S&P500 bounced convincingly off the 100-day MA at the end of last month and now looks to be moving out of its recent range, having consistently closed above the 55-day Moving Average all this week. If prices can close above 3431, then bulls will set their sights on the all-time highs at 3587.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.